What Are Common Mistakes to Avoid on IRS Form 8849?

Form 8849 is one of those IRS documents that looks deceptively simple until you are the one trying to defend a refund claim with real dollars attached. Whether you are a fuel distributor, a logistics operator, or an employer dealing with specialty excise items, the biggest Form 8849 errors usually come from process gaps, not math.

Below are the most common mistakes to avoid on IRS Form 8849 (Claim for Refund of Excise Taxes), plus practical strategies that finance teams use to reduce rework, delays, and IRS correspondence.

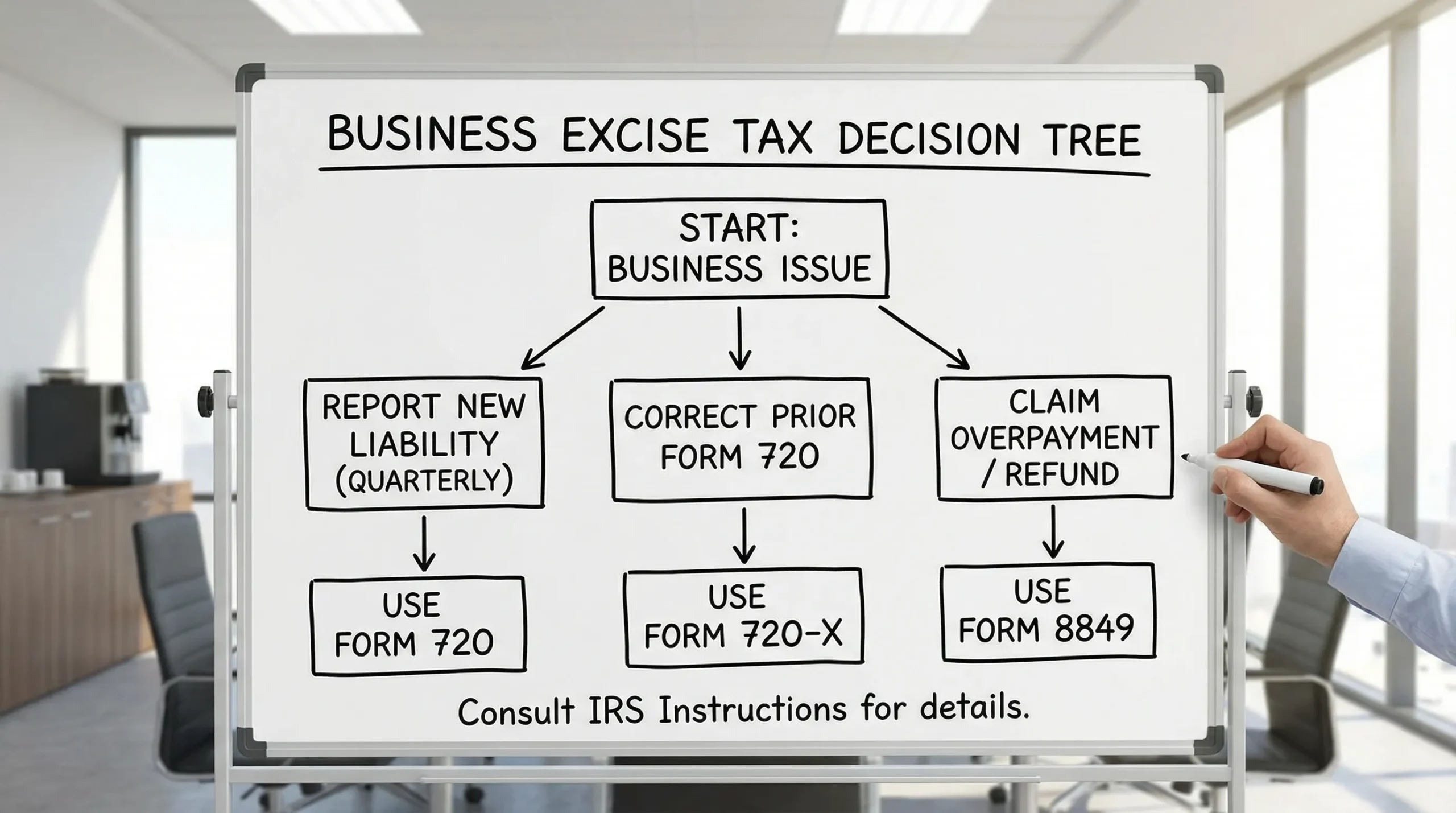

First, where Form 8849 fits (and why it is easy to misuse)

Form 8849 is used to claim certain excise tax refunds or credits. It often connects to taxes reported on Form 720, but it is not the same thing as correcting a filed return.

A quick mental model:

- Form 720 reports liability (what you owe).

- Form 720-X corrects a prior Form 720.

- Form 8849 claims a refund (often with schedule-specific documentation).

Mistakes happen when teams pick the wrong tool, or when the claim does not reconcile to the way liability was originally reported.

For official references, start with the IRS source documents: Form 8849 and the Instructions for Form 8849.

Common mistake #1: Using Form 8849 when you should amend Form 720 (or vice versa)

A classic error is treating Form 8849 as a universal fix for any excise tax issue. In practice, the IRS expects the form that matches the action.

| Situation | Correct path (typical) | Why it matters |

|---|---|---|

| You underreported excise tax on a prior quarter | Form 720-X | You are correcting a return, not claiming a stand-alone refund |

| You overreported and want a refund tied to that quarter | Form 720-X or Form 8849 (depends on tax type/schedule rules) | Wrong form can lead to delays or an IRS letter |

| You are claiming a specific statutory refund (for example, certain fuel claims) | Form 8849 with the right schedule | Many claims require schedule-level details and supporting records |

PCORI Fee specific pitfall

The PCORI Fee is reported on Form 720 (typically once per year, even though Form 720 is a quarterly return). One common mistake is attempting to “refund” PCORI via the wrong mechanism without aligning to IRS instructions for corrections. If your PCORI situation changed, confirm the appropriate correction path in the Form 720 instructions and your advisor.

Common mistake #2: Filing the wrong schedule (or leaving schedule fields incomplete)

Most Form 8849 claims are schedule-driven, and the schedule is not just a checkbox. It determines:

- What tax you are claiming

- Which documentation is expected

- How the IRS will validate timelines and eligibility

Teams often get tripped up by:

- Selecting the wrong schedule for the tax type

- Mixing claim types that should be separated

- Leaving required identifiers blank (registrations, product codes, transaction details)

Strategic fix: Treat schedule selection like a compliance control. Build a “claim mapping” worksheet that ties each claim line back to the excise category and the source transaction type.

Common mistake #3: Claim timing problems (missing the window or claiming the wrong period)

Refund claims are highly sensitive to dates, including when the tax was paid, when the underlying event occurred, and when the claim is filed.

Timing errors often look like:

- Claiming a period outside the allowed window

- Using invoice dates when the rule requires payment or usage dates

- Claiming quarterly patterns that do not match how the business actually remits or reports on Form 720

Strategic fix: Add a “date governance” step before submission. Require the preparer to document which date field controls eligibility (invoice date vs. removal date vs. payment date) and store it with the claim file.

Common mistake #4: Not reconciling Form 8849 amounts to Form 720 reporting

Even when Form 8849 is technically correct, mismatches with Form 720 tend to trigger questions.

Reconciliation problems commonly come from:

- Different internal owners preparing Form 720 vs. Form 8849

- Using different source systems (ERP vs. fuel card statements vs. manual spreadsheets)

- Netting credits in one place but grossing them up in another

Here is a simple “close-like” reconciliation framework that experienced tax teams use:

| Control step | What you compare | What it catches |

|---|---|---|

| Tax code mapping check | Form 720 line items vs. Form 8849 schedule categories | Wrong tax category, wrong schedule |

| Period alignment | Quarter/year covered by the claim vs. quarter/year reported | Off-by-one quarter issues |

| Source-to-return tie-out | Transaction totals vs. claim totals | Missing transactions, duplicates |

Common mistake #5: Weak documentation (especially on fuel-related claims)

Many Form 8849 claims are only as strong as the receipts behind them. A frequent reason claims get slowed down is not having a clean, auditable package.

Documentation gaps include:

- Missing invoices, bills of lading, or usage logs

- No clear explanation of why the excise tax was paid and why it is refundable

- Inconsistent quantities or units of measure (gallons, pounds, units)

- Not retaining proof of payment and proof of eligible use

Strategic fix: Build a standard “claim binder” (digital is fine) with consistent naming and an index. This is also helpful in diligence scenarios.

Investor lesson learned (diligence reality)

In private equity and acquisition diligence, refund claims can look like “free money” on a working-capital model until the buyer asks for support. One common lesson from PE-backed operators is that the value of a pipeline of excise refunds depends on documentation quality and claim defensibility, not the headline dollar amount.

Common mistake #6: Entity and identification errors (the IRS cannot match your claim)

Form 8849 processing can stall when the IRS cannot reliably match the claimant to prior filings.

Watch for:

- EIN/name mismatch vs. prior Form 720 filings

- Using the wrong filer (parent vs. subsidiary)

- Address inconsistencies that break IRS matching

Strategic fix: Lock down a single “taxpayer profile” record and reuse it consistently across Form 720, Form 720-X, and Form 8849.

Common mistake #7: Treating Form 8849 like a one-person task instead of a controlled workflow

The most expensive mistakes are repeatable ones.

A simple operating model that reduces errors:

- One owner for tax logic (eligibility, schedule selection)

- One owner for data and reconciliation

- One reviewer (not the preparer) for completeness and ID matching

This is where an organized filing workflow and support can matter. E Eile Excise 720 (eFileExcise720) is an IRS-authorized platform focused on excise compliance, including Form 8849 claims support, secure handling, and guided navigation for the broader Form 720 ecosystem.

If you are also trying to confirm Who Needs to File Form 720, align that determination first because it affects how you document liabilities, deposits, and the downstream refund story.

A quick “error rate” reality check (why process matters)

The IRS has pushed electronic filing for years, and adoption is extremely high across many return types. For context, IRS Data Book reporting has shown that over 90% of individual returns are e-filed in recent years, reflecting a broad trend toward digital submission and automated validation. See the IRS Data Book for the latest figures.

Even though Form 8849 workflows are not the same as individual e-file, the operational lesson carries over: standardized data, validation checks, and consistent documentation reduce downstream friction.

Comparing two real-world operating approaches (and what happens)

Approach A: “Refund-chasing”

A venture-backed mobility company notices excise taxes embedded in vendor billing and rushes Form 8849 filings whenever cash gets tight. They file quickly, but cannot tie claims cleanly to supporting transactions. Result: more IRS correspondence, longer time to cash, and messy audit trails.

Approach B: “Refund as a controlled receivable”

A sponsor-backed fleet operator treats refunds like AR. They reconcile each claim to the underlying tax logic and maintain a standard binder. Result: fewer resubmissions, cleaner diligence support, and better predictability when forecasting cash.

The difference is not sophistication, it is repeatable controls.

Where “pricing” and support fit into the strategy

Many teams wait until they are already late, already rejected, or already responding to a notice before looking for tooling and support.

If you are evaluating help, do not just compare pricing. Compare:

- Whether the provider is IRS-authorized (for applicable e-file services)

- How well the workflow reduces missing data and mismatches

- Whether support can help you route correctly between Form 720, 720-X, and Form 8849

On eFileExcise720, you can review pricing and, if you are unsure how to proceed, contact us for guidance on the right filing path for your situation.

Quick questions people ask before filing

Can I use tax form 8849 to correct a mistake on a Form 720 I already filed? Often, corrections to a filed Form 720 are handled with Form 720-X. Form 8849 is generally for specific refund claims. Confirm using IRS instructions for your tax type.

Is irs form 8849 only for fuel tax refunds? No. Fuel claims are common, but Form 8849 also supports other excise tax refund scenarios depending on the schedule and eligibility rules.

Does the PCORI Fee belong on form 8849? Typically, PCORI Fee reporting happens on Form 720. If you need to correct PCORI reporting, verify the proper correction method in IRS guidance and consider professional advice.

If I do not know Who Needs to File Form 720, should I still submit a Form 8849 claim? Clarify your Form 720 filing requirement first because it affects how your excise positions are reported and documented.

Where can I get help if my claim is rejected or I am unsure about schedules? You can use an excise-focused platform like E Eile Excise 720 (eFileExcise720) and contact us for support on form selection, documentation readiness, and next steps.