What Is Ship Passenger Tax? A Complete Guide for Cruise Operators

Cruise pricing is often marketed as “all-in,” but behind every itinerary is a stack of taxes, fees, and compliance work that can materially affect margins and cash flow. One of the most commonly misunderstood items is the federal Ship Passenger Tax. If you operate cruise itineraries touching U.S. ports, understanding this tax is not optional, it is a recurring operational requirement that can scale quickly with passenger volumes.

This guide answers the core question, What Is Ship Passenger Tax, and then goes further with practical filing strategy, controls cruise finance teams use to avoid surprises, and how investors think about these “small per-passenger” obligations when they compound across sailings.

What is Ship Passenger Tax (and where it comes from)

The U.S. federal Ship Passenger Tax is an excise tax imposed under Internal Revenue Code sections 4471 and 4472. In general terms, it applies per passenger on certain voyages of commercial passenger vessels where passengers embark or disembark in the United States.

- Statute reference: 26 U.S.C. § 4471 and 26 U.S.C. § 4472

- Filing mechanism: typically reported on IRS Form 720 (Quarterly Federal Excise Tax Return)

The headline rate (why it adds up faster than it looks)

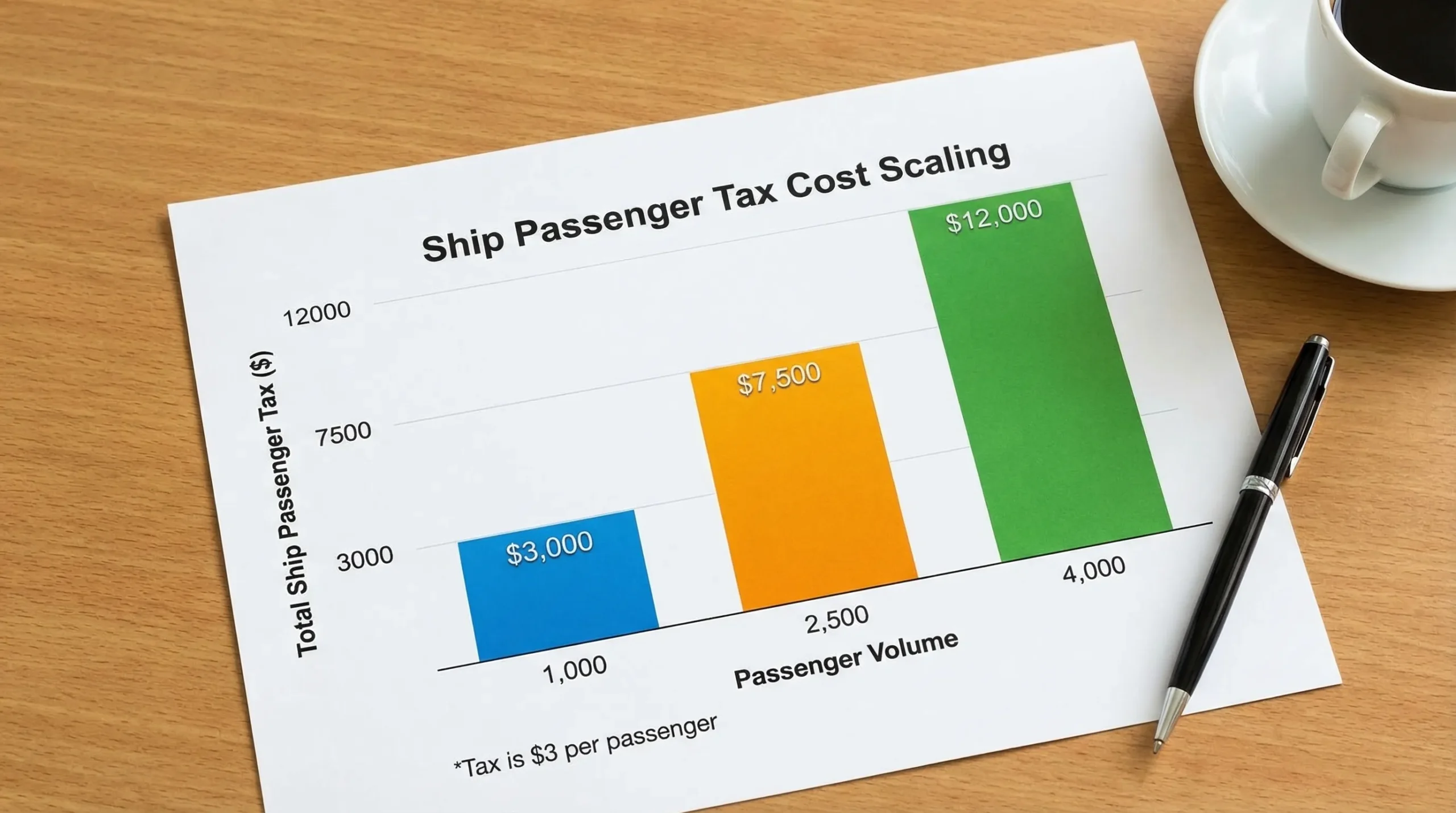

The tax is commonly described as $3 per passenger on covered voyages. That sounds minor until you multiply it by modern ship capacity and sailing frequency.

Here is a simple “how big can this get?” view that finance teams often use when budgeting:

| Operating scenario (illustrative) | Passengers per sailing | Sailings per year | Estimated Ship Passenger Tax at $3 per passenger |

|---|---|---|---|

| Small vessel, seasonal schedule | 700 | 30 | $63,000 |

| Mid-size ship, steady schedule | 2,000 | 40 | $240,000 |

| Large ship, weekly sailings | 4,000 | 50 | $600,000 |

Those totals are not “industry averages,” they are simple math. The point is that this excise tax becomes a real line item once operations scale.

Who is responsible for paying and reporting it

For most cruise operators, the party responsible for reporting and paying the Ship Passenger Tax is the operator of the commercial passenger vessel (and in some cases, the owner or an authorized agent depending on operational structure).

This matters for:

- Bareboat or time charter structures where the commercial operator may not be the legal owner.

- Management companies running vessels for multiple brands.

- Foreign operators using U.S. agents.

From a governance perspective, investors and lenders typically want comfort that the entity collecting ticket revenue also has strong tax compliance controls, because excise taxes are transactional and can trigger penalties if missed.

What counts as a “covered voyage” and a “taxable passenger”

The Ship Passenger Tax hinges on statutory definitions (not marketing labels like “closed-loop cruise”). In broad terms, it generally involves:

- A commercial passenger vessel.

- A covered voyage as defined in the law.

- Passengers who embark or disembark in the United States under the covered-voyage rules.

Because eligibility can turn on itinerary facts (ports, where passengers get on or off, and how the voyage is structured), many operators treat this as an “itinerary plus manifest” tax and build controls around those two datasets.

If you are designing an internal policy, align your tax determination to:

- The statutory language in IRC 4471/4472.

- The latest IRS instructions for Form 720 and any related guidance.

- Your passenger accounting definitions (who is “on manifest,” who is complimentary, who is crew, who is onboard for partial segments, etc.).

How to calculate Ship Passenger Tax (a practical operating view)

While legal definitions control, the practical workflow in cruise accounting usually looks like this:

- Identify covered voyages during the quarter that trigger the tax.

- Determine the count of taxable passengers tied to those voyages based on embarkation/disembarkation events covered by the rules.

- Apply the per-passenger rate.

- Reconcile to operational systems and ticketing.

A useful control for scale operators is a reconciliation that ties out three numbers:

- Passenger manifest totals (operations)

- Passenger ticket revenue counts (commercial)

- Taxable passenger counts (tax)

When those three don’t agree, the “gap” is often where filing errors or overpayments happen.

Ship Passenger Tax filing on Form 720 (quarterly cadence)

Ship Passenger Tax is generally reported on Form 720, which is filed quarterly. Form 720 is the IRS’s primary return for federal excise taxes across many categories.

If your business also has other excise responsibilities, you may already have a Form 720 process for items like:

- The PCORI Fee (reported annually on Form 720 in many cases, often referred to as the pcori 720 form or form 720 pcori in internal checklists)

- Transportation-related excise taxes

- Environmental and fuel-related excise taxes

That comparison is strategic: PCORI is annual and HR-driven, ship passenger tax is voyage-driven and operationally tied to port cycles. Merging them into one “excise calendar” reduces the risk of missing a quarter.

What about a Zero Liability Return?

Cruise operators sometimes ask whether they should file a Zero Liability Return (a Form 720 showing no tax due) in quarters without covered voyages. In general, many taxpayers only file Form 720 for quarters in which they have liability, but filing expectations can vary based on IRS account setup and business facts. If you are unsure whether a zero filing is appropriate for your entity, confirm with a tax professional or reference the current Form 720 instructions.

Amendments, overpayments, and when Form 8849 comes up

Two tools matter when correcting excise tax issues:

- Form 720-X is typically used to amend or make adjustments to previously filed Form 720 amounts.

- Tax Form 8849 (also searched as 8849 form or IRS Form 8849) is used to claim refunds for certain excise taxes in specific situations.

For cruise teams, the strategic takeaway is not “which form do I prefer,” it is this: build your quarter-close process to minimize corrections in the first place by locking down passenger counts and voyage classifications before you file.

You can review IRS basics here: About Form 8849.

Strategic advice: what sophisticated operators do (and what investors notice)

The ship passenger tax itself is straightforward in rate, but operational complexity is where most risk sits. Here are patterns seen in mature operators and the “lessons learned” that often emerge after an internal audit or lender diligence.

1) Treat it like a revenue system control, not a tax spreadsheet

The strongest compliance setups pull taxable passenger counts from controlled systems (manifest and port call data) and apply rule logic consistently. Spreadsheets still exist, but they are reconciliations, not the source of truth.

2) Build an itinerary review step into schedule planning

Voyage design decisions can change tax exposure. Even when the dollar amount is not huge, consistency matters because:

- Errors repeat quickly across weekly sailings.

- Excise mistakes create penalty and interest exposure.

3) Document assumptions the same way every quarter

Investors tend to discount companies when “small but frequent” compliance items show up as surprises. Public cruise operators routinely discuss taxes and regulatory compliance as a risk factor in their disclosures, not because ship passenger tax alone is existential, but because repeated compliance issues signal weak controls.

A simple internal memo template can help:

- What itineraries were treated as covered voyages

- Data source for passenger counts

- Who approved the final taxable passenger number

- Where supporting reports are stored

4) Plan for cash flow timing

Even if you collect taxes through ticketing and remit later, you still need clean quarter-end cutoffs, especially when sailings cross quarter boundaries.

Filing Ship Passenger Tax online (and reducing preventable errors)

If you want faster confirmation, clearer tracking, and less manual handling, many operators move Ship Passenger Tax Filing Online through an authorized e-file provider.

E Eile Excise 720 (eFileExcise720) is an IRS-authorized platform for e-filing Form 720 that supports Form 720 categories and provides secure handling and customer support. If ship passenger tax is one of several excise items you manage (for example, if your company also files PCORI on Form 720), consolidating your workflow into one e-filing process can simplify compliance.

You can learn more or start here: eFileExcise720.