Foreign Insurance Tax Explained: Who Must Pay and Why It Matters

Foreign Insurance Tax is one of those compliance items that often stays invisible until it becomes expensive. It can apply even when a company is doing everything “right” from an insurance perspective, for example buying specialty coverage from the London market or placing reinsurance with a non-US carrier. Then, during an audit or a deal, someone realizes a federal excise tax may have been due all along.

This guide explains what the Foreign Insurance Tax is, who must pay it, and why it matters strategically (especially for growing companies, cross-border coverage, and M&A). It also shows how it’s reported on Form 720 and what to do if you need to correct past filings.

What is Foreign Insurance Tax (and where it comes from)

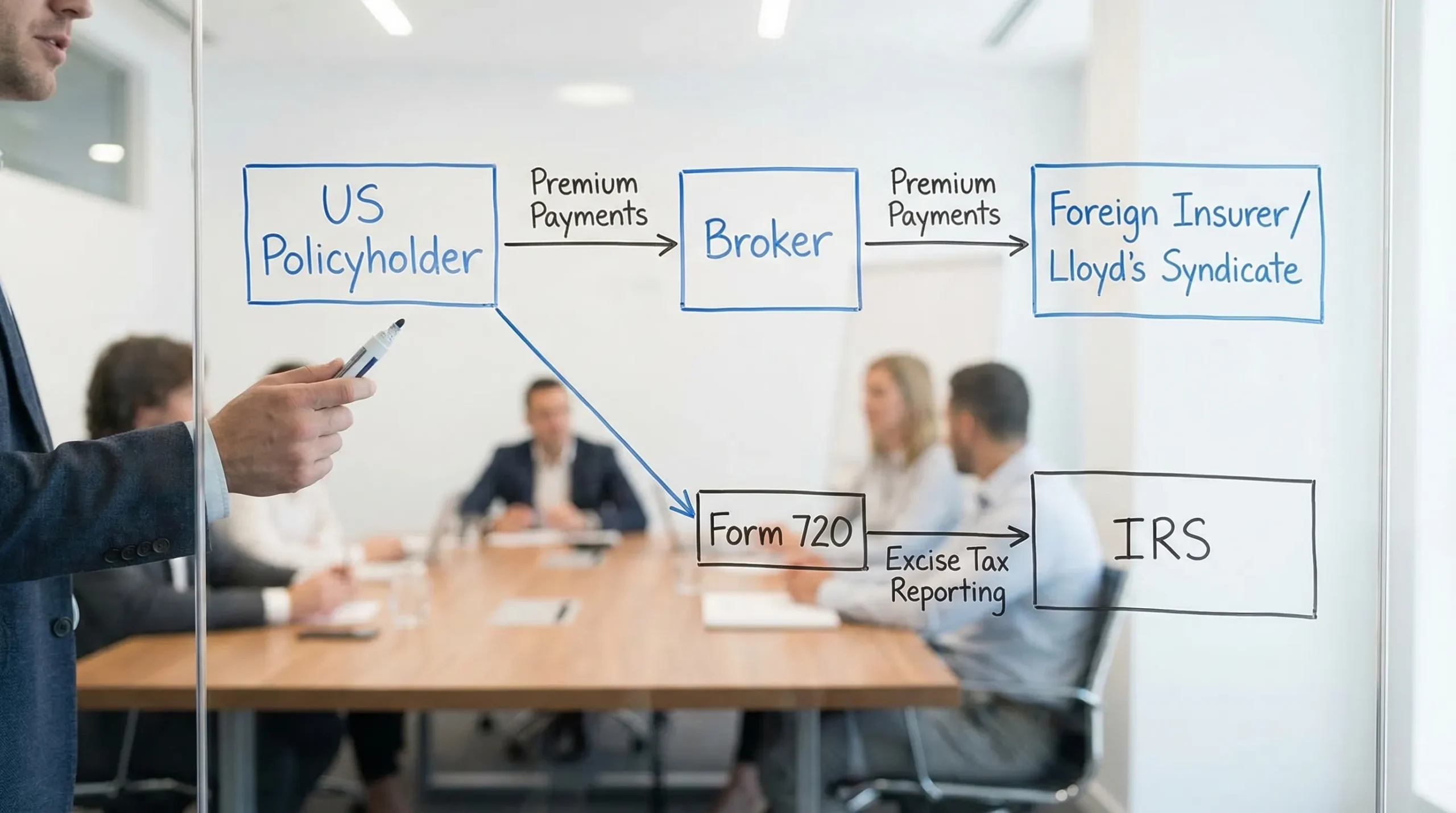

“Foreign Insurance Tax” generally refers to the federal excise tax on insurance policies issued by foreign insurers under Internal Revenue Code Section 4371. The concept is straightforward: if the insurer (or reinsurer) is foreign and the policy covers US risks, the IRS may assess an excise tax on the premium.

Practical reality is less straightforward because modern insurance programs can involve:

- Brokers and intermediaries

- Layered programs with multiple carriers

- Foreign reinsurance backing a US-issued policy

- Policies covering multi-country operations with allocated premiums

The tax is typically reported on IRS Form 720 (Quarterly Federal Excise Tax Return). See the IRS’s Form 720 overview and the statutory language at 26 U.S. Code § 4371.

Who must pay Foreign Insurance Tax?

In many cases, the liability falls on the person who makes the premium payment to the foreign insurer (or to an intermediary for that foreign insurer). That “person” might be:

- The US policyholder (common in commercial placements)

- A broker paying the carrier on behalf of the insured

- Another entity in the payment chain, depending on how the transaction is structured

Because the “payer” can vary, Foreign Insurance Tax is a frequent due diligence item in acquisitions and roll-ups. Buyers want to know whether the target has been handling excise taxes correctly, especially if it uses foreign markets for D&O, cyber, marine, or specialty liability.

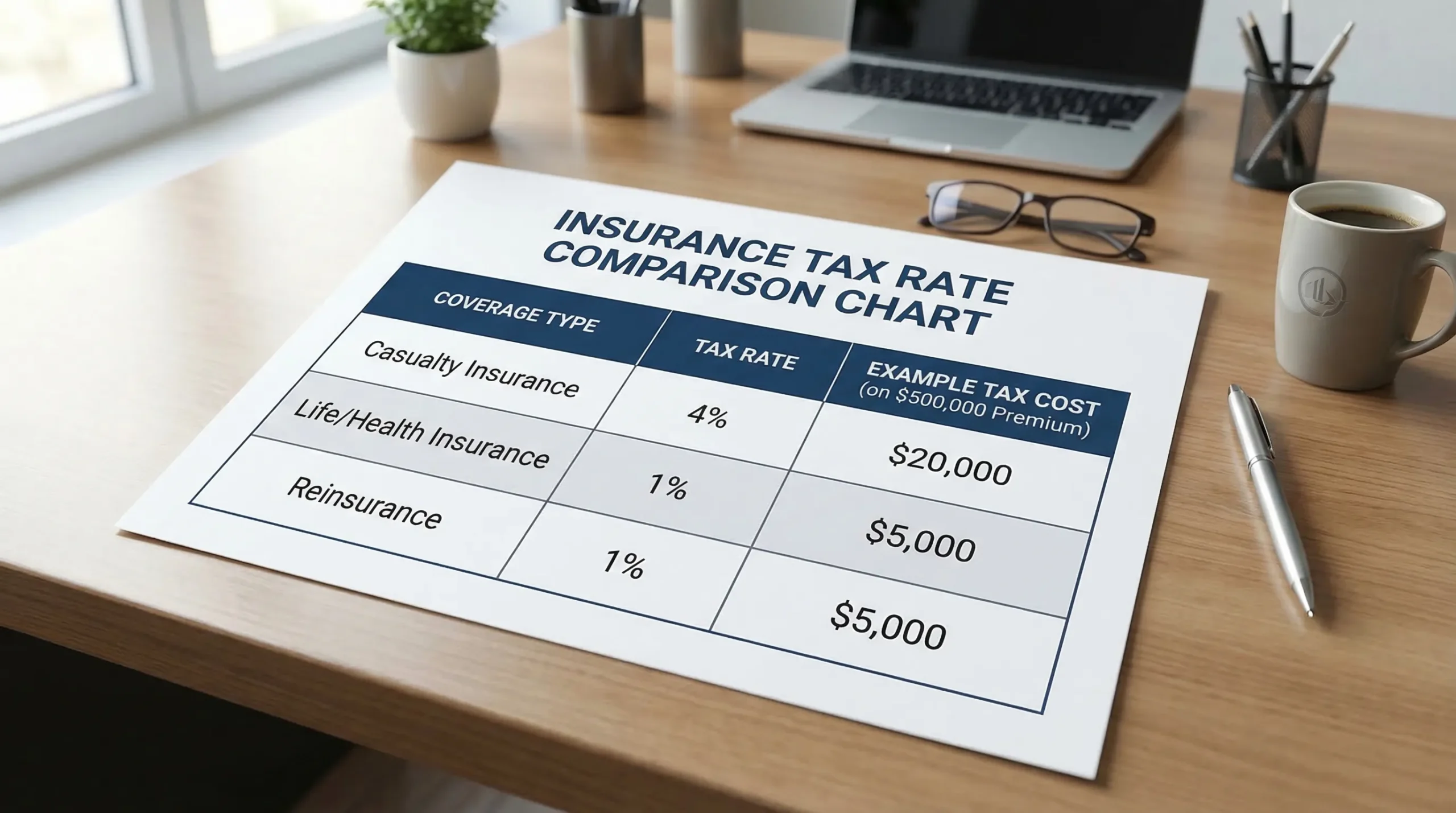

The core tax rates (what you actually pay)

The Foreign Insurance Tax rate depends on the type of coverage.

| Coverage type (simplified) | Common description | Typical excise tax rate |

|---|---|---|

| Casualty insurance and indemnity bonds | Many commercial P&C coverages | 4% |

| Life, sickness, accident | Life and certain health-related coverages | 1% |

| Reinsurance | Premiums paid to foreign reinsurers | 1% |

Always validate classification with the Form 720 instructions and your tax advisor. Misclassification is one of the easiest ways to overpay or underpay.

Why it matters in 2026: trends and business risk

Foreign Insurance Tax is not just a “tax form detail.” It affects cost, controls, and deal outcomes.

1) Cross-border and specialty insurance buying is more common

Companies increasingly buy coverage that is hard to place domestically or is priced more competitively via foreign markets (often via the London market, Bermuda-based capacity, or global programs). The more your insurance program globalizes, the easier it is for excise tax ownership to get unclear.

2) Small misses can become big numbers

Because the tax is a percentage of premium, it scales quickly.

| Annual premium paid to a foreign insurer | 1% tax (life/reinsurance) | 4% tax (casualty) |

|---|---|---|

| $100,000 | $1,000 | $4,000 |

| $500,000 | $5,000 | $20,000 |

| $2,000,000 | $20,000 | $80,000 |

Now layer in multiple policy years, penalties, and interest. This is why investors care: a “small” compliance gap can become a material purchase price issue.

3) It is often confused with state-level charges

Foreign Insurance Tax is federal. Many companies already pay state-level charges like surplus lines taxes or stamping office fees. These are different obligations.

| Item | Level | What triggers it | Is it the same as Foreign Insurance Tax? |

|---|---|---|---|

| Foreign Insurance Tax (IRC 4371) | Federal | Premium paid to foreign insurer/reinsurer for US risks | No |

| Surplus lines tax | State | Placement with non-admitted insurer | No |

| Premium tax | State | Admitted insurance premiums | No |

A company can owe one, two, or (in some structures) multiple charges. Treating one payment as “covering everything” is a common and costly assumption.

Strategic lessons learned (investor-style examples)

Below are real-world style scenarios commonly seen in diligence. They are anonymized composites, but the patterns are familiar to PE and corporate development teams.

Example A: PE-backed roll-up with a “global” D&O policy

A private equity platform buys three add-on companies. The parent had D&O coverage placed through a foreign market, with premiums paid via a broker. Accounting assumed the broker handled all related taxes.

What diligence teams often uncover in similar situations:

- Surplus lines taxes were paid at the state level.

- Foreign Insurance Tax was not reported on Form 720 because ownership was unclear.

Outcome: the buyer requires a holdback or specific indemnity until historical exposure is quantified and corrected.

Example B: Venture-backed company buys cyber coverage offshore

A fast-growing technology company buys cyber coverage where a portion of the program is issued by a foreign insurer due to capacity constraints. Premium is allocated across multiple jurisdictions.

Common operational gap:

- Premium allocation schedules exist (from the broker), but they are not mapped into quarterly excise tax compliance.

Outcome: the company adds a control: every renewal triggers a “taxability review” and a quarterly checklist item for Foreign Insurance Tax.

How Foreign Insurance Tax fits into Form 720 compliance

Foreign Insurance Tax is reported on Form 720, which is also used for many other excise taxes. That matters because businesses often already touch Form 720 for other reasons, such as:

- PCORI Fee reporting (sometimes searched as “pcori 720 form” or “form 720 pcori”)

- Communication and Air Transportation Tax filing Online

- Fuel, environmental, or manufacturing excise items

So, strategically, the best time to fix Foreign Insurance Tax compliance is when you standardize your overall quarterly excise process.

If you truly have no liability for a quarter across your applicable categories, some filers ask about a Zero Liability Return. Whether you should file a zero return depends on your facts and filing history (and any IRS requirements tied to prior filings). If you are unsure, confirm with a tax professional.

Corrections, amendments, and refunds (Form 720-X and Form 8849)

If you discover an error after filing, correction options typically include:

- Form 720-X to amend previously filed Form 720 returns

- In certain excise tax situations, Form 8849 (often searched as tax form 8849 or irs form 8849) is used to claim refunds or credits

Important nuance: Form 8849 is schedule-driven and is not a universal refund form for every excise tax scenario. Use it only when your claim clearly fits the schedules and instructions. The IRS’s Form 8849 page is the best starting point.

Practical compliance checklist (the 15-minute version)

If you want Foreign Insurance Tax to stop being a “surprise category,” build a lightweight control:

- Confirm whether any policies involve foreign insurers, Lloyd’s syndicates, or foreign reinsurance

- Identify who actually pays the premium (insured, broker, captive, parent company)

- Map premiums to US risk exposure where allocations exist

- Classify the coverage type (4% vs 1% is a big swing)

- Tie renewal dates to quarterly reporting so nothing falls between teams

When you are ready to file, an IRS-authorized e-file workflow can reduce basic errors and improve documentation. eFileExcise720 is built to support Form 720 categories in one place, and E Eile Excise 720 (as some customers refer to it) is commonly used by businesses that want a simpler way to manage quarterly excise compliance online.

FAQ: Foreign Insurance Tax

Who is responsible for paying Foreign Insurance Tax? Usually the person who pays the premium to the foreign insurer (or to an intermediary for that insurer). In practice, this may be the insured or a broker, depending on the payment chain.

Do I report Foreign Insurance Tax on Form 720? Yes, it is commonly reported on IRS Form 720 as part of quarterly federal excise tax reporting.

Is Foreign Insurance Tax the same as surplus lines tax? No. Surplus lines tax is generally state-level, while Foreign Insurance Tax is federal under IRC 4371. You may owe one or both depending on your placement.

If I already file the PCORI Fee on Form 720, does that help? Yes. If you already file Form 720 for the PCORI Fee, adding Foreign Insurance Tax becomes a process and documentation issue, not a brand-new filing obligation.

Can I use Form 8849 to claim back Foreign Insurance Tax? Form 8849 is used for certain excise tax refund claims, but it is schedule-specific. Confirm eligibility under the Form 8849 instructions or consult a tax professional.