Electronic Filing for IRS: Benefits, Limits, and Proof

Electronic filing has moved from “nice to have” to “default expectation” in tax operations. For excise tax filers in particular, electronic filing for IRS can reduce preventable rejects, tighten your compliance timeline, and create cleaner documentation when you need to prove you filed on time or support a refund claim.

But e-filing is not magic. It has limits, and the difference between a smooth quarter and an expensive cleanup often comes down to one thing: proof.

Below is a practical, strategy-first guide to e-filing IRS excise forms like Form 720, handling PCORI Fee reporting on the pcori 720 form, and managing refund claims on the 8849 form (also referred to as the tax form 8849).

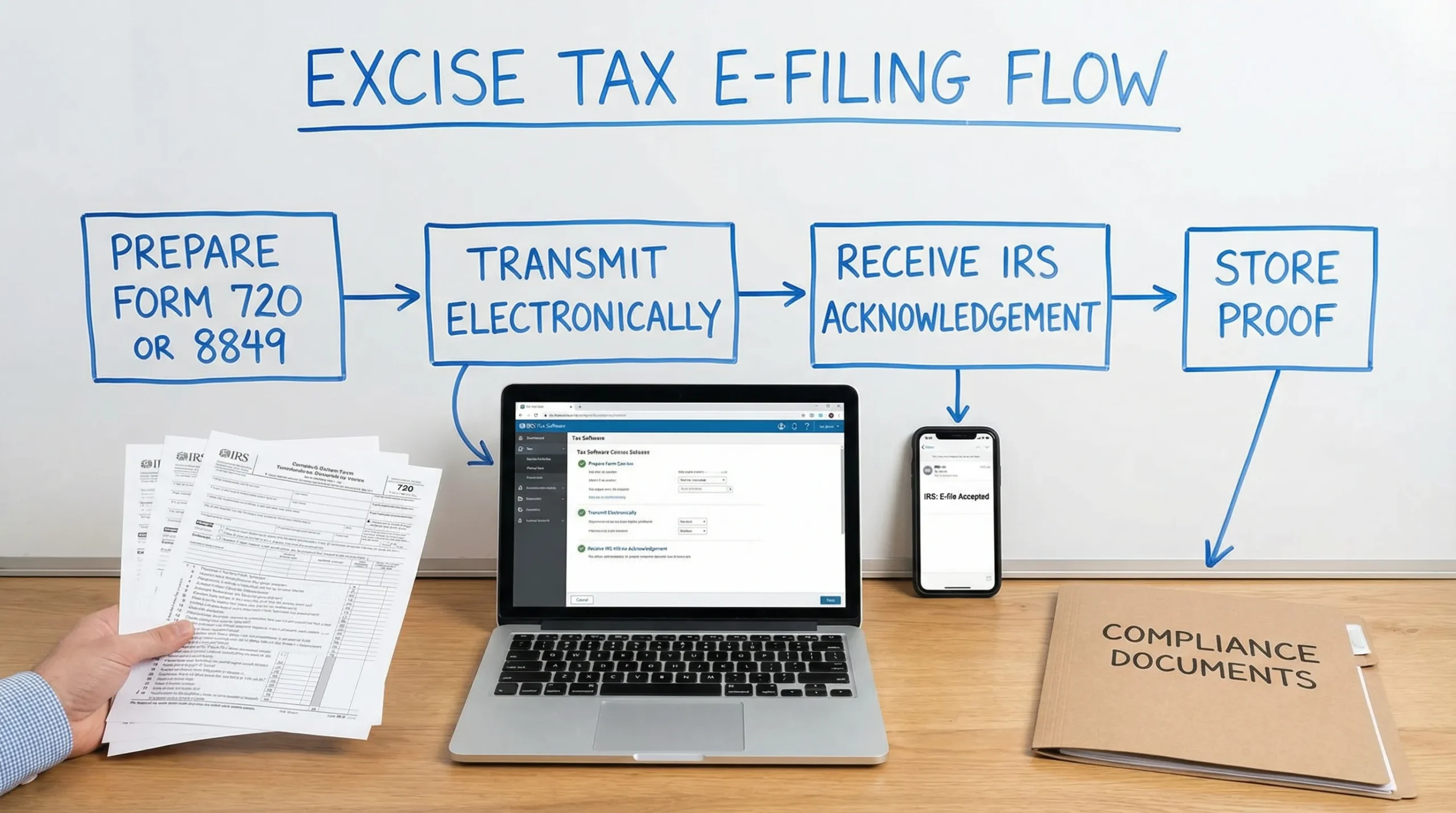

What “electronic filing for IRS” means for excise tax filers

For many income tax filers, e-file means a direct consumer workflow. Excise tax is different. Form 720 (Quarterly Federal Excise Tax Return) and claims like Form 8849 (Claim for Refund of Excise Tax) are typically e-filed through IRS-authorized providers rather than through a simple IRS “upload” page.

That matters because your operational risk shifts from “Did we mail it?” to:

- Did we transmit successfully?

- Did the IRS accept it?

- Can we prove acceptance and payment timing later?

Platforms like E Eile Excise 720 (eFileExcise720) are built specifically around this excise workflow, including Form 720 categories, amendments (Form 720-X), and Form 8849 claims support.

Benefits: why e-filing wins in the real world

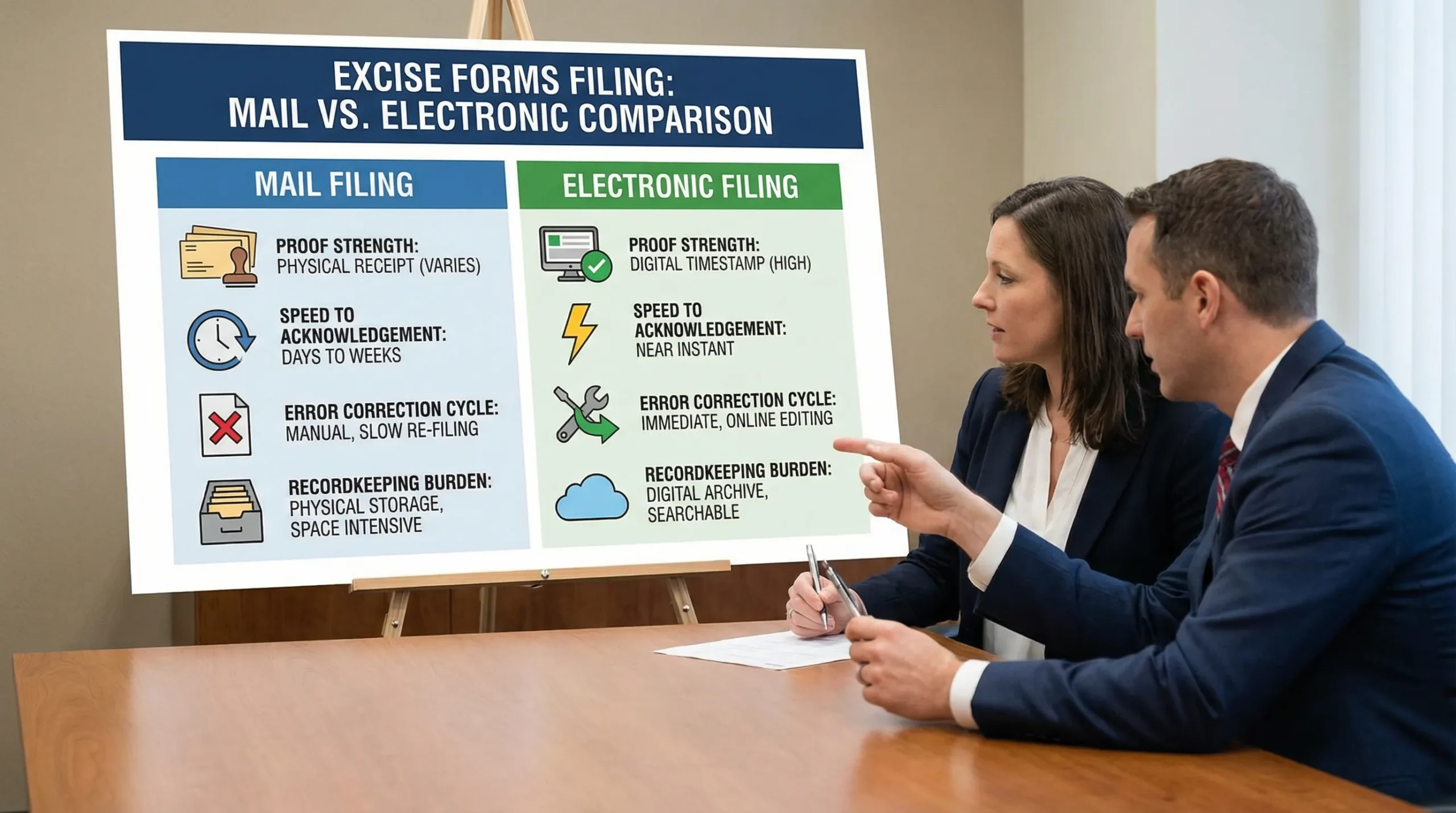

1) Stronger proof of timely filing

With paper filing, your best proof is usually a postmark, tracking number, and delivery confirmation. With e-file, you can often create a cleaner audit trail: transmission details, acceptance/rejection acknowledgements, and electronic payment records.

This is not just administrative. Late filing can get expensive quickly. The IRS explains failure-to-file and failure-to-pay penalties and how they may apply (see IRS penalty overview). Even if you ultimately file correctly, weak proof can turn a “we filed” conversation into a “prove it” problem.

2) Faster error detection (and fewer compounding mistakes)

Excise filings can fail for avoidable reasons: mismatched EIN/name control, quarter selection errors, math issues, or missing schedules. E-file systems typically surface these sooner than a mailed form that sits in a processing queue.

3) Better cash-flow control for claims and credits

If you file Form 8849 for eligible refunds (depending on schedule and your excise category), the operational win is less about “instant refunds” and more about clean submission packages that reduce back-and-forth.

To understand what Form 8849 is used for and which schedules apply, refer to the IRS form and instructions and a dedicated explainer like eFileExcise720’s Form 8849 overview.

Limits: what e-filing does not solve

Electronic filing for IRS is powerful, but you still need controls around the process.

E-file does not fix bad inputs

If your source data is wrong, the return can still be wrong, just faster. Common root causes include:

- Pulling the wrong quarter for form 720 liabilities

- Using an incorrect IRS number/tax rate mapping

- Inconsistent documentation behind a tax form 8849 claim

E-file does not eliminate timing risk

You can still miss deadlines if your team waits until the last day, hits a reject, and cannot resolve it before the cut-off. Treat e-file like a pipeline with checkpoints, not a last-minute button.

Not every edge case is “one-click”

Some situations require extra documentation, careful reconciliation, or professional review (for example, complex fuel claims, entity changes, or corrections after acceptance).

Proof: the “3 receipts” model you should store

If you want to make e-filing defensible, store proof like you expect a future reviewer to ask, “Show me.”

| Proof item | What it shows | Why it matters |

|---|---|---|

| Submission record | When you transmitted, and what was sent | Establishes a timeline and version control |

| IRS acknowledgement (accepted/rejected) | Whether the IRS accepted the filing | Acceptance is usually the key “proof” event |

| Payment confirmation (if applicable) | When/how payment was initiated and settled | Supports penalty defense and reconciliation |

Strategy tip: Save these artifacts in a quarterly “close” folder alongside your workpapers, not inside someone’s email.

Trend watch (2026): e-file is becoming the compliance baseline

Across tax functions, the trend is consistent: more digital processing, more structured data, and less patience for missing documentation. For excise filers, that means your competitive advantage is not only filing electronically, it is having a repeatable system:

- Standardized data inputs per excise line

- Acknowledgement capture and retention

- A claims register for anything filed on form 8849

Think of this like an internal control environment. Investors and lenders increasingly care about tax compliance hygiene because it reduces contingent liabilities during diligence.

How to Amend Form 8849 (practical approach)

“Amending” Form 8849 is a common way people describe fixing a claim, but the IRS process is typically handled as a corrected or subsequent claim rather than a simple checkbox that says “amended.” Always follow the official instructions for your specific schedule and claim type.

Here is a practical, low-drama approach many tax teams use:

1) Identify what changed and why

Be explicit: was it gallons, dates, vendor documentation, taxable use, or a schedule selection issue? The goal is to create a narrative a reviewer can follow.

2) Rebuild the claim package

For many 8849 form schedules, the strength of your supporting documentation determines whether the IRS comes back with questions. Reconcile your corrected figures to source documents and keep a clean workpaper trail.

3) Submit a corrected claim in a controlled way

Avoid “patching” numbers without a record. Instead:

- Prepare the corrected tax form 8849 based on the right schedule

- Reference the original filing internally (date, period, confirmation/acknowledgement)

- Keep both versions and the explanation memo together

4) Update your claims register

Maintain a simple log: claim type, amount, submission date, acknowledgement date, and resolution status. This one control prevents duplicated claims and missed follow-ups.

If you’re filing excise returns and claims together, consider consolidating your workflow so Form 720 liabilities, Form 720-X adjustments, and Form 8849 claims are tracked in one place.

Two “investor-style” examples (composite lessons)

These are composite examples (not specific clients), but they reflect patterns seen in excise compliance.

Example A: PE-backed transportation operator using Form 8849

A private-equity-backed fleet expanded quickly through acquisitions. The tax team filed Form 8849 claims but lacked consistent proof packages by entity. In diligence, the investor’s operating team requested support for each claim.

Lesson learned: e-filing helps, but the real win is standardizing the proof bundle (submission, acceptance, support, reconciliation) per EIN.

Example B: High-growth employer with PCORI Fee on Form 720

A venture-backed company moved from fully insured to partially self-insured benefits and became responsible for the PCORI Fee. The team filed the form 720 pcori reporting but struggled to document covered lives methodology.

Lesson learned: e-file gives faster confirmation, but you still need a repeatable calculation memo and retained inputs.

Frequently Asked Questions

What is the best proof that I filed electronically with the IRS? The strongest proof is the IRS acknowledgement showing “accepted,” plus your transmission record and payment confirmation (if you paid with the filing).

Is Form 720 required for the PCORI Fee? Yes, the PCORI Fee is reported on Form 720 (often informally called the pcori 720 form), even if you do not file Form 720 for other excise taxes.

How to Amend Form 8849 if I made a mistake? In practice, you usually file a corrected or subsequent claim (following the Form 8849 instructions for your schedule), keep the original acknowledgement, and document exactly what changed.

Can I e-file Form 8849 and Form 720? Many filers can e-file these through an IRS-authorized provider. Eligibility can depend on your situation and the form schedules involved.

What records should I keep for a tax form 8849 claim? Keep the filed form, the IRS acknowledgement, and the supporting documentation used to compute the claim (plus a reconciliation showing how you arrived at the amounts).

File electronically with an IRS-authorized excise e-file provider

If you want electronic filing for IRS excise returns with a clearer audit trail, E Eile Excise 720 (eFileExcise720) is an IRS-authorized platform designed for Form 720, Form 720-X, and Form 8849 workflows. You can create a free account, e-file without downloading software, and get dedicated support along the way.

Explore options at eFileExcise720 or review the Form 8849 claim guide to plan your next filing with better proof and fewer surprises.