Form 720 Penalty for Late Filing: What Businesses Need to Know

Late filing IRS Form 720 is one of those “small admin misses” that can quickly turn into a measurable financial hit. The IRS can assess penalties for filing late, penalties for paying late, and interest on unpaid amounts, and those charges can compound while your team is busy running operations.

For businesses that treat excise taxes as a quarterly checklist item, the real risk is not just the penalty percentage. It is the downstream friction: vendor compliance questions, financing diligence, and extra work to unwind mistakes through amendments or refund claims.

The basics: what “late” means for Form 720

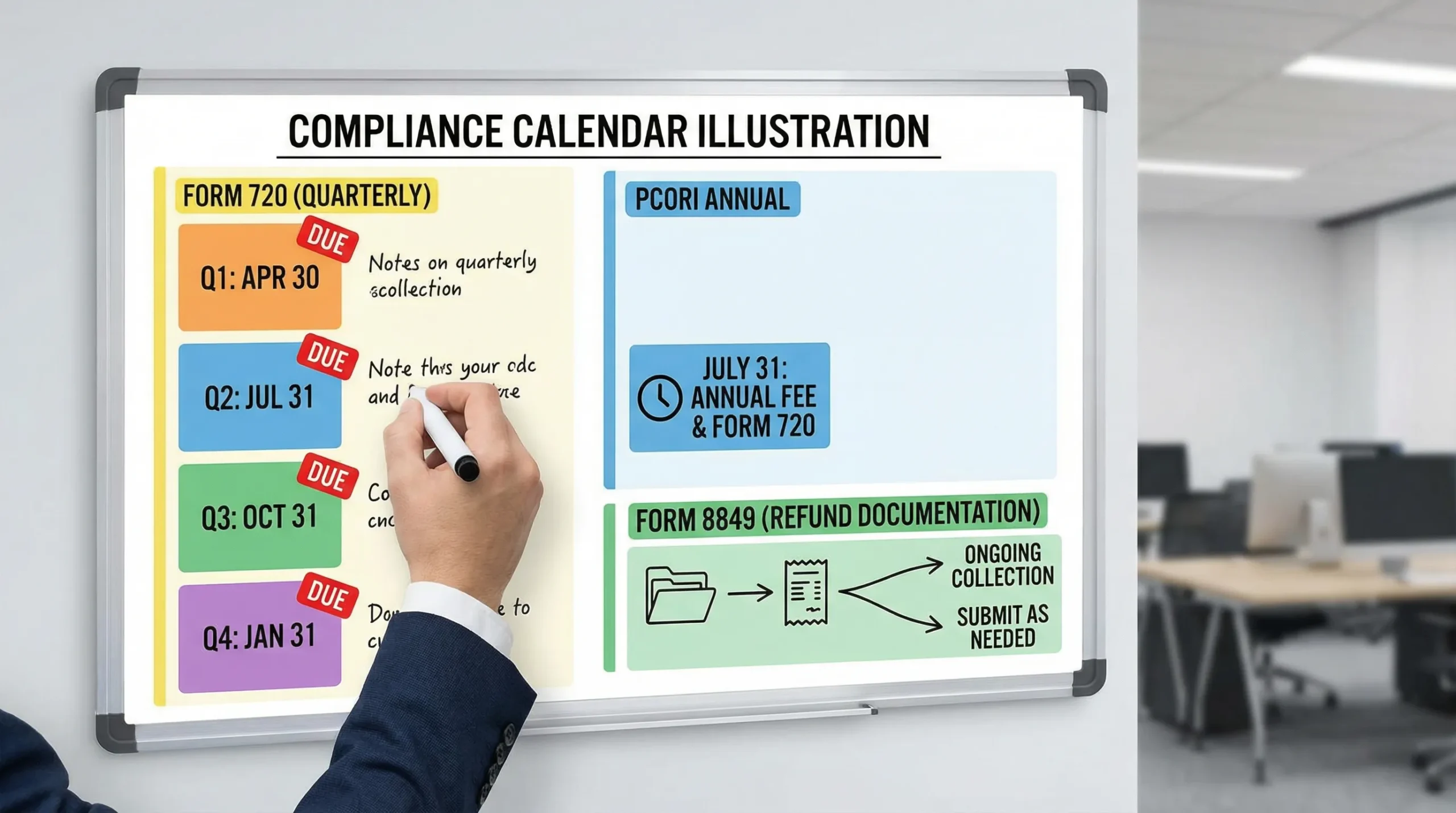

Form 720 is a quarterly federal excise tax return. In most cases, it is due by the last day of the month following the end of the quarter (for example, Q1 is generally due April 30). If your filing is submitted after the due date and you owe tax, you are in late-filing territory.

Two reminders that trip up otherwise organized finance teams:

- If you owe excise tax, the IRS generally cares about timely filing and timely payment. Filing “soon” is not the same as filing on time.

- Some filers are also subject to deposit rules (often via EFTPS). Deposit errors can create additional penalties separate from the return itself.

For the IRS’ general overview of penalty types, see IRS Penalties.

How the IRS penalties add up (plus interest)

While specifics can vary by situation, two common penalty buckets businesses encounter are:

- Failure-to-file penalty (often calculated as a percentage of unpaid tax per month, up to a cap)

- Failure-to-pay penalty (often calculated as a smaller percentage of unpaid tax per month, up to a cap)

Interest is also charged on unpaid tax and, in many cases, on penalties. The IRS updates interest rates periodically, so treat interest as a moving input rather than a fixed percentage.

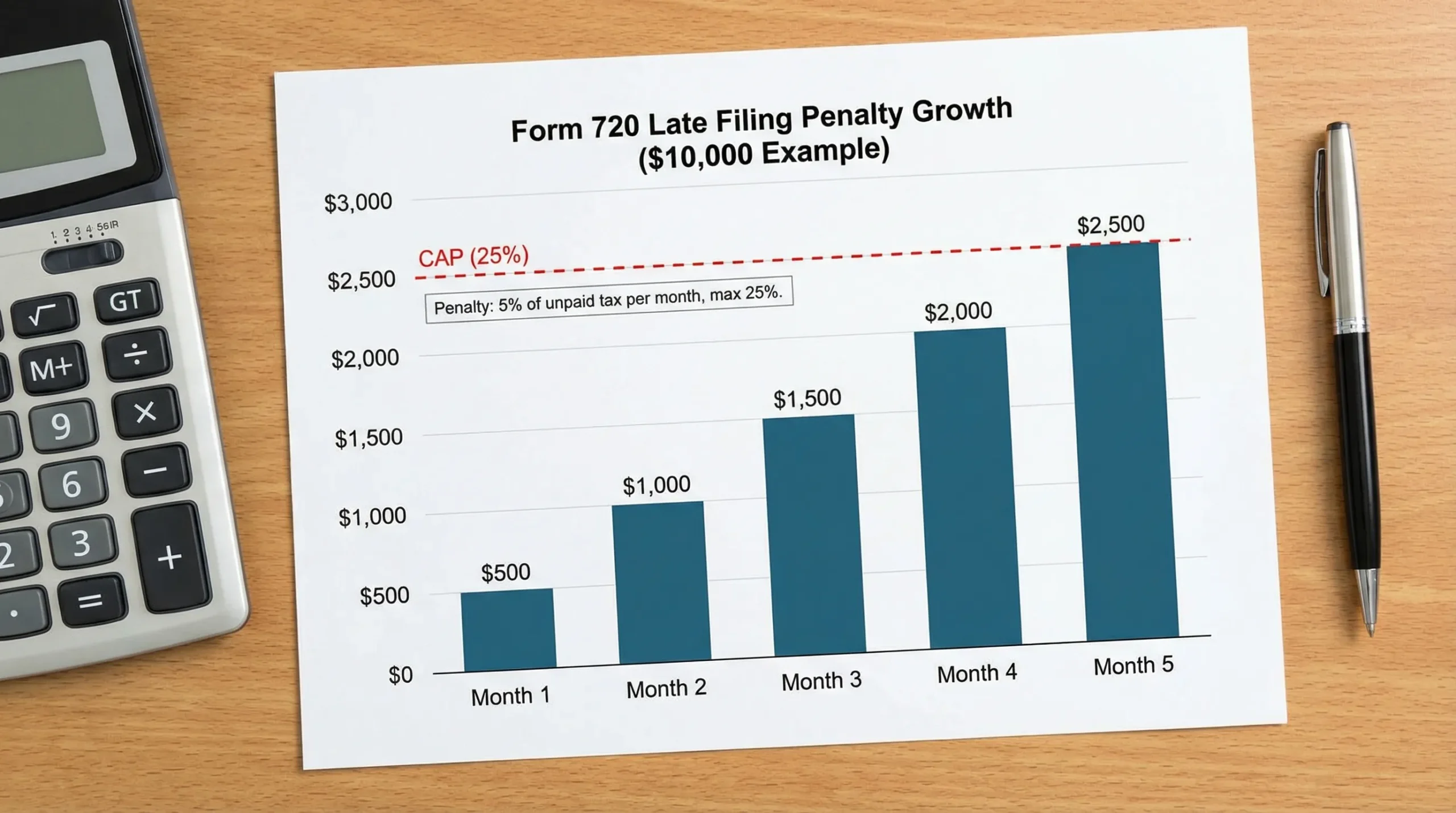

A practical penalty “chart” to model exposure

The table below shows a simple modeling view for a business that owes $10,000 in excise tax and files late. This illustrates the failure-to-file penalty at a commonly referenced 5% per month (capped at 25%). It does not include failure-to-pay penalties or interest, which can further increase the total.

| Months late | Illustrative failure-to-file penalty rate | Illustrative penalty on $10,000 | What it means operationally |

|---|---|---|---|

| 1 | 5% | $500 | Your “quarterly close” miss becomes a real cost line item. |

| 2 | 10% | $1,000 | Penalties start to rival the effort cost of better controls. |

| 3 | 15% | $1,500 | Cash flow pressure increases if you are also catching up deposits. |

| 4 | 20% | $2,000 | Late filing becomes a diligence question, not just a tax issue. |

| 5+ | 25% (cap) | $2,500 | The cap helps, but interest and other penalties can keep growing. |

Takeaway: even modest excise tax liabilities can become meaningful once you layer in compounding charges and internal rework time.

Why investors and lenders care about Form 720 lateness

Late excise compliance is increasingly viewed as a process quality signal, especially in industries where excise taxes are embedded in pricing, fuel usage, imports, or benefits administration.

Here is what tends to happen in real diligence workflows (especially for investor-backed or acquisition-minded companies):

- Quality of earnings adjustments: recurring penalties may be treated as non-operational add-backs, but they still raise the question, “What else is missing?”

- Working capital stress: if late filings coincide with under-accruals, the company can get hit with an unexpected cash requirement.

- Reps and warranties pressure: buyers may ask for stronger tax reps, escrow holdbacks, or special indemnities when they see late Form 720 patterns.

Lessons learned from investor-style scenarios (examples)

These are common patterns that show up in mid-market diligence, without relying on any single company’s confidential details:

- Private equity owned logistics operator: The finance team filed quarterly, but fuel-related excise mapping changed after a systems migration. The business filed one quarter late while reconciling data, and the combined penalties plus interest became an avoidable “transaction distraction” during a refinancing.

- Growth-stage employer with self-insured benefits: PCORI Fee reporting was treated as an HR task, not a tax task. The team missed the annual filing tied to the pcori 720 form, then had to correct the workflow while responding to internal audit questions.

- Construction services vendor with fleet operations: Job costing tracked fuel spend, but not always the taxability context. Operationally, firms doing site services like street sweeping services in Nashville may run equipment usage patterns that make excise documentation and refund support more complex than a general ledger can show.

PCORI Fee is a frequent “surprise” late-filing trigger

The PCORI Fee is one of the most common reasons otherwise non-excise-heavy businesses end up filing Form 720. Many organizations only touch Form 720 for PCORI once per year, which increases the risk of:

- missing the due date because it is not part of the normal quarterly tax calendar

- miscounting covered lives (or using the wrong counting method)

- assigning ownership to the wrong team (benefits, payroll, or accounting)

Strategic fix: treat PCORI like a mini “tax close.” Set a recurring internal deadline, document the counting method, and keep support in a single shared location.

If you overpaid, can Form 8849 help reduce the damage?

Sometimes late filing happens alongside a separate realization: you overpaid excise tax earlier in the year, or you have a legitimate credit/refund position (often fuel-related). That is where a form 8849 claim for refund of excise taxes can matter.

Key point: a refund claim does not automatically erase late filing penalties on a different period or different liability. But refund strategy can still improve cash flow while you clean up compliance.

Form 720 vs 8849 form vs 720-X (quick comparison)

| Form | Primary purpose | Typical use case | Common risk |

|---|---|---|---|

| Form 720 | Report and pay quarterly excise tax | Ongoing excise liability (fuel, environmental, communications, PCORI, etc.) | Late filing and payment penalties if missed |

| 8849 form (tax form 8849) | Claim refund/credit of certain excise taxes | Qualified fuel uses, exports, certain credits | Wrong schedule or weak documentation delays refund |

| Form 720-X | Amend a previously filed Form 720 | Correct reporting errors for a quarter already filed | Misstating the adjustment period or tax line |

If you are trying to fix late compliance and improve cash flow, talk to your tax advisor about whether a tax form 8849 filing is appropriate, and ensure your refund position is supported with audit-ready documentation.

What to do right now if you missed the deadline

When businesses search for Late Form 720 Filing Online, the best move is usually speed plus accuracy:

- File the return as soon as possible (waiting rarely helps)

- Pay as much as you can as soon as you can (to reduce ongoing charges)

- Gather support for the numbers you report, especially if you expect follow-up questions

- If the reason was truly outside your control, ask your tax professional about potential penalty relief options

Prevent it next quarter: a simple operating system for excise compliance

Excise taxes are increasingly operational, not just accounting. A practical control framework looks like this:

- Monthly accrual check: even if you file quarterly, review taxable activity monthly.

- Source-to-line mapping: document which internal reports feed each Form 720 line item.

- Ownership clarity: assign a single owner for Form 720 and a backup.

- Refund playbook: if you regularly file Form 8849, standardize schedules, substantiation, and retention.

Tools matter here. An IRS-authorized e-file provider can reduce timing risk by giving you a structured workflow and submission acknowledgments.

How eFileExcise720 fits into a lower-risk filing strategy

If your goal is to reduce late-filing exposure, eFileExcise720 is designed to streamline excise compliance with:

- IRS-authorized e-filing

- Free account creation and no software download

- Secure data protection

- Simple dashboard navigation

- Support for Form 720 categories, amendments (720-X), and Form 8849 claims

For businesses that value reliable tax return filing services, the operational win is consistency: fewer missed deadlines, fewer preventable errors, and faster resolution when you need to correct or claim.

Frequently Asked Questions

What is the penalty for filing Form 720 late? The IRS can assess a failure-to-file penalty (often calculated monthly as a percentage of unpaid tax, up to a cap), plus interest and potentially other penalties depending on your situation.

If I file Form 720 late but pay in full, do I still owe penalties? You may still owe a late-filing penalty even if you pay quickly, although paying sooner can reduce additional charges like interest and late-payment penalties.

Does the PCORI Fee use Form 720? Yes. The PCORI Fee is reported on Form 720 (often referred to as the pcori 720 form in practice), which is a common reason employers file even if they have no other excise taxes.

When should I use the 8849 form instead of Form 720? Use the 8849 form (tax form 8849) when you are eligible to claim a refund or credit of certain excise taxes. Form 720 is generally for reporting and paying the excise tax liability.

Can a form 8849 claim for refund of excise taxes reduce my late filing penalties? Not automatically. A refund claim may improve cash flow, but late filing penalties generally relate to the period and unpaid tax on the late return.

File now, reduce risk next quarter

If you need to catch up or want a repeatable process to avoid penalties, you can file Form 720 online with eFileExcise720 at efileexcise720.com. E-filing can help you submit faster, reduce common errors, and keep your excise compliance on a predictable quarterly cadence.