Fuel Excise Tax Filing in California

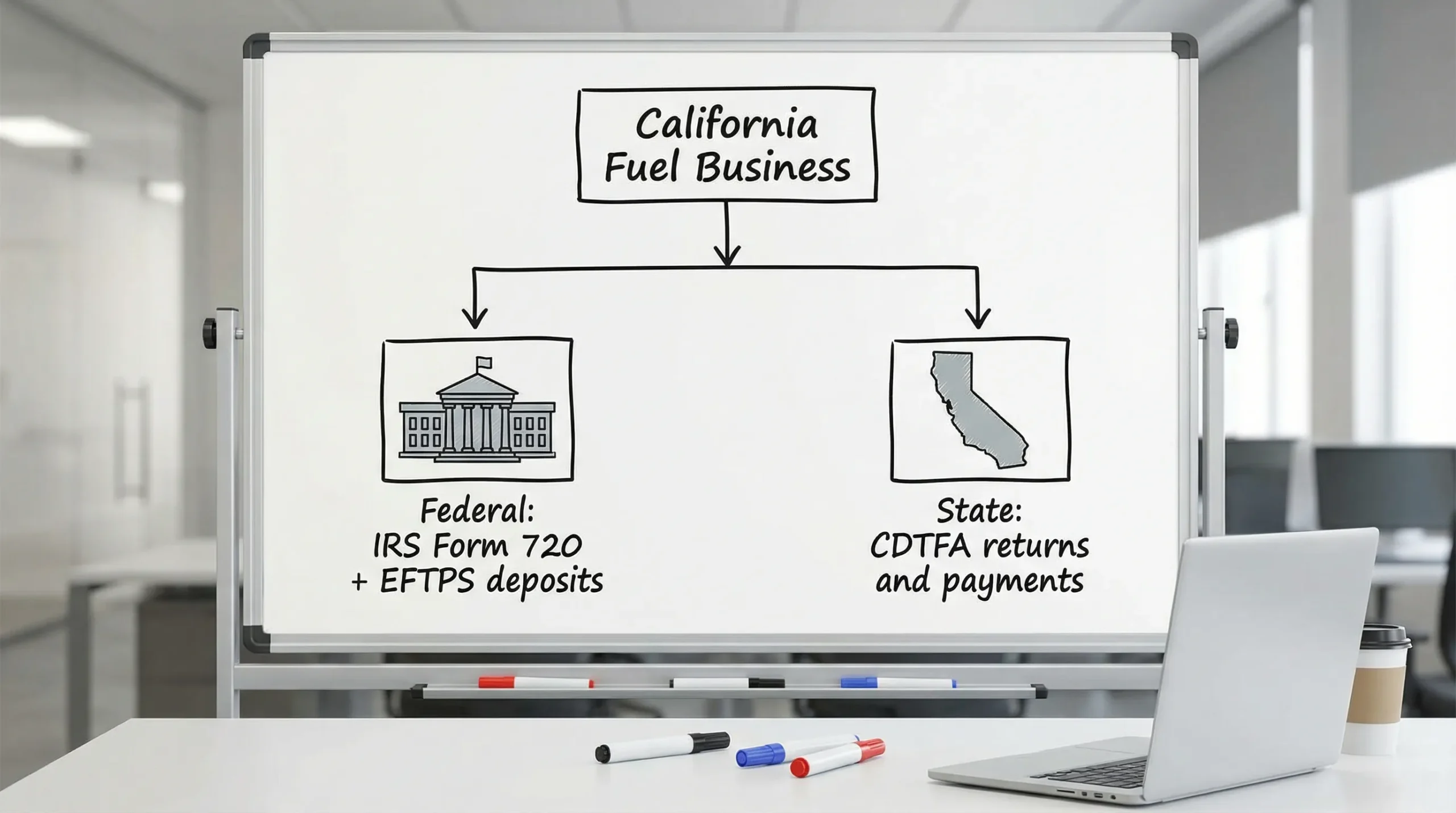

Fuel excise tax in California generally refers to taxes imposed on fuel transactions, but it is crucial to separate California state fuel tax from federal fuel excise tax. At the federal level, many fuel excise tax liabilities are reported to the IRS on Form 720 (Quarterly Federal Excise Tax Return) and may also require federal fuel tax deposits through EFTPS. At the state level, California fuel taxes are administered by the California Department of Tax and Fee Administration (CDTFA), with separate registrations, returns, and rules. If you operate in California, you may have both federal and CDTFA obligations depending on your role in the fuel supply chain.

California fuel tax vs federal fuel excise tax (Form 720)

California businesses often search for “fuel tax California” or “Form 720 California” when they are trying to stay compliant across multiple agencies. Here is the clean split you need for accurate filing.

Federal fuel excise tax (IRS Form 720)

Federal fuel excise tax is reported to the IRS primarily on Form 720 when you have taxable fuel activities, such as certain removals, entries, sales, or uses of taxable fuel.

Federal compliance may also involve:

- EFTPS payments for semimonthly fuel tax deposit obligations (when required)

- Schedule reporting within Form 720 (for example, Schedule A for deposit liabilities, depending on your activity)

- Adjustments, credits, or refunds, when eligible (often involving Form 8849 claims and/or Form 720-X amendments)

Official reference: IRS Form 720 page and EFTPS.

California state fuel tax (CDTFA)

California state fuel tax obligations are administered by the CDTFA (and may involve other state agencies depending on the fuel program). These are not filed on IRS Form 720.

CDTFA responsibilities commonly include state-level licensing, reporting, and payment requirements for fuel taxpayers operating in California.

Official reference: CDTFA.

Who must file in California

If you do business in California, you may need Form 720 filing CA support if your operations trigger federal fuel excise tax. This often applies to fuel supply chain participants, not just retailers.

You may have a federal Form 720 filing requirement if you are a:

- Fuel producer, refiner, blender, or importer

- Terminal operator, position holder, or other party involved in fuel removals/entries

- Distributor, wholesaler, or reseller with taxable fuel transactions

- Fleet operator or business with specialized taxable uses, or that needs to claim credits/refunds

You may also need CDTFA filing/registration if you:

- Conduct fuel distribution or wholesale activities in California

- Import, export, or deliver fuel into California channels

- Operate in categories CDTFA regulates for state fuel tax reporting

Compliance tip: “E-file fuel tax California” searches often reflect confusion between agencies. IRS Form 720 is federal, CDTFA filings are state, and your business may be responsible for both.

Common taxable fuel activities in CA (federal Form 720 focus)

For federal purposes, fuel excise tax liability is generally triggered by specific taxable events tied to taxable fuels (commonly including gasoline, diesel fuel, kerosene, and certain alternative fuels, depending on facts and product classification).

Common federally taxable fuel activities that California operators should watch include:

- Removal of taxable fuel under circumstances that create tax

- Entry of taxable fuel (such as into the U.S.) under taxable conditions

- Certain sales or uses of fuel that the IRS treats as taxable

- Situations involving dyed fuel and disallowed uses (fact-specific)

- Alternative fuel transactions that are taxable or creditable, depending on the fuel and use

If you are dealing with California diesel tax or gasoline excise tax CA at the state level, do not assume the same rules apply federally. Federal taxability is determined under IRS excise rules, and reporting is done through Form 720 when required.

Filing deadlines and deposit schedules

Fuel excise compliance is usually time-sensitive because it can involve both:

- A quarterly return filing requirement (Form 720)

- A deposit requirement during the quarter (often semimonthly) when thresholds and rules apply

Form 720 due dates (federal)

Form 720 is filed quarterly. The due date is the last day of the month following the end of the quarter.

| Form 720 quarter | Period covered | Typical due date |

|---|---|---|

| Q1 | Jan 1 to Mar 31 | Apr 30 |

| Q2 | Apr 1 to Jun 30 | Jul 31 |

| Q3 | Jul 1 to Sep 30 | Oct 31 |

| Q4 | Oct 1 to Dec 31 | Jan 31 |

If a due date falls on a weekend or legal holiday, the deadline typically moves to the next business day (per IRS rules).

Federal fuel tax deposits (EFTPS)

Many fuel excise taxpayers must make federal fuel tax deposits during the quarter via EFTPS, rather than waiting to pay everything with the quarterly return.

Key points that apply to many fuel filers:

- Deposits are commonly semimonthly (twice per month) when required.

- Deposit timing is tied to the semimonthly period and is generally due shortly after the period ends.

- The IRS has special timing rules for certain September deposit periods.

Because deposit rules are fact-specific, many businesses use a compliance process that separates:

- Transaction capture and classification (by IRS category)

- Deposit liability tracking

- Quarterly reconciliation and e-filing

Practical payment reference: EFTPS enrollment and payment guidance.

California (CDTFA) due dates

CDTFA fuel tax returns and payment frequencies depend on your account type and program. If you have CDTFA registration, follow the filing calendar and notices issued for your account.

Penalties for non-compliance

Fuel excise tax penalties can compound quickly when you miss deposits, file late, or report incorrectly.

Federal penalties (IRS)

Federal risk typically falls into three categories:

- Failure to file Form 720 on time

- Failure to pay the tax shown as due

- Failure to make required deposits on time (when deposit rules apply)

The IRS can also assess interest on late amounts. For a baseline overview of federal excise filing concepts, see the IRS and Form 720 instructions: IRS Form 720.

California penalties (CDTFA)

CDTFA can assess penalties and interest for late returns, late payments, or compliance issues tied to state fuel tax programs.

If you operate across federal and California programs, align your internal calendar so quarterly Form 720 work does not distract from CDTFA due dates.

Compliance note: This page provides general information, not legal or tax advice. For guidance on your exact facts, consult a qualified tax professional.

How eFileExcise720 simplifies fuel excise tax filing in California

If your goal is California fuel excise tax filing on the federal side, the fastest path is usually accurate preparation plus an IRS-authorized e-file workflow.

eFileExcise720 is an IRS-authorized e-file provider built to streamline Form 720 compliance for fuel filers and other excise taxpayers.

Here is what that means for California businesses, distributors, and fleet operators:

- IRS-authorized e-filing for Form 720 so you can submit online without printing and mailing.

- Free account creation and no software download needed, useful for teams filing from multiple locations.

- Supports all Form 720 categories, including fuel schedules and excise categories beyond fuel.

- Secure data protection designed for sensitive taxpayer and transaction information.

- Personalized customer support for filing workflow questions and reject resolution.

- Amendments and claims support, including Form 720-X amendments and Form 8849 claims workflows when applicable.

If you searched “Form 720 California” or “e-file fuel tax California,” the core value is simple: file the federal return correctly and on time, while keeping your CDTFA workstream separate and organized.

Fuel excise filing plus other excise taxes (same portal)

Many California operators file fuel excise tax and also have other excise obligations during the year. eFileExcise720 supports multiple excise categories so you can keep compliance consolidated.

Examples include:

- PCORI fee reporting using IRS Form 720 PCORI (often searched as “irs form 720 pcori” or “720 pcori form”)

- Other quarterly excise categories reported on Form 720

If you need to switch from fuel to another excise category later in the year, you do not want a new system every time.

What to prepare before you e-file Form 720 (California fuel businesses)

To reduce IRS rejects and speed up filing, prepare these items before you start your Form 720 filing CA workflow:

- Your business legal name, EIN, and current address (match IRS records)

- The quarter you are filing for, and whether you have deposit liabilities

- Fuel transaction totals by product and taxable activity category (based on how the IRS requires reporting)

- Any credit or refund support documents if you are filing a claim or adjustment (potentially relevant for Form 8849 situations)

- Your payment method plan, including EFTPS if deposits apply

If you are unsure whether your activity is taxable, do not guess. Misclassification is a common cause of notices.

Frequently Asked Questions

What is the difference between California fuel tax and federal fuel excise tax? California fuel tax is a state obligation administered by the California Department of Tax and Fee Administration (CDTFA). Federal fuel excise tax is administered by the IRS and is commonly reported on IRS Form 720, with deposits often paid through EFTPS.

Do I file California fuel excise tax on Form 720? Not for California state fuel tax. Form 720 is a federal IRS return. California state fuel tax filings are handled through CDTFA, using CDTFA registrations and returns.

Who needs Form 720 filing in CA for fuel? California businesses that trigger federal taxable fuel activities, such as certain removals, entries, sales, or uses of gasoline, diesel, kerosene, or alternative fuels, may need to file IRS Form 720 even if they also file CDTFA returns.

What is a semimonthly fuel tax deposit and how do I pay it? A semimonthly fuel tax deposit is a federal excise tax deposit schedule that may apply to certain fuel excise taxpayers. When required, deposits are generally made electronically through EFTPS based on the IRS semimonthly periods.

Can I e-file Form 720 in California? Yes. You can e-file Form 720 through an IRS-authorized provider. eFileExcise720 is an IRS-authorized e-file platform that supports Form 720 categories, including fuel, and helps you submit online.

How do Form 720-X and Form 8849 relate to fuel excise tax? Form 720-X is used to amend a previously filed Form 720. Form 8849 is used to claim certain refunds of excise taxes, depending on eligibility and the specific claim type. Your facts determine which form applies.

File your federal fuel excise taxes online (California)

If your business needs federal fuel excise compliance, do not wait until the quarterly deadline to discover you also had deposit obligations.

File accurately, on time, and with a clear audit trail using an IRS-authorized workflow.

- Create your account and start your Form 720 e-file now: eFileExcise720

- Need to correct a prior quarter? Use Form 720-X support through the same portal.

- Claiming eligible credits or refunds? eFileExcise720 supports Form 8849 filing workflows.

Ready to e-file fuel tax for your California operation? Get started here: File Form 720 online.