IRS Form 720 PCORI Filing Guide for 2026

For many employers and benefits administrators, PCORI filing is a once-a-year Form 720 task that is easy to overlook. The return itself is quarterly, but the PCORI fee is reported annually, and the due date is tied to the plan or policy year that ended in the prior calendar year.

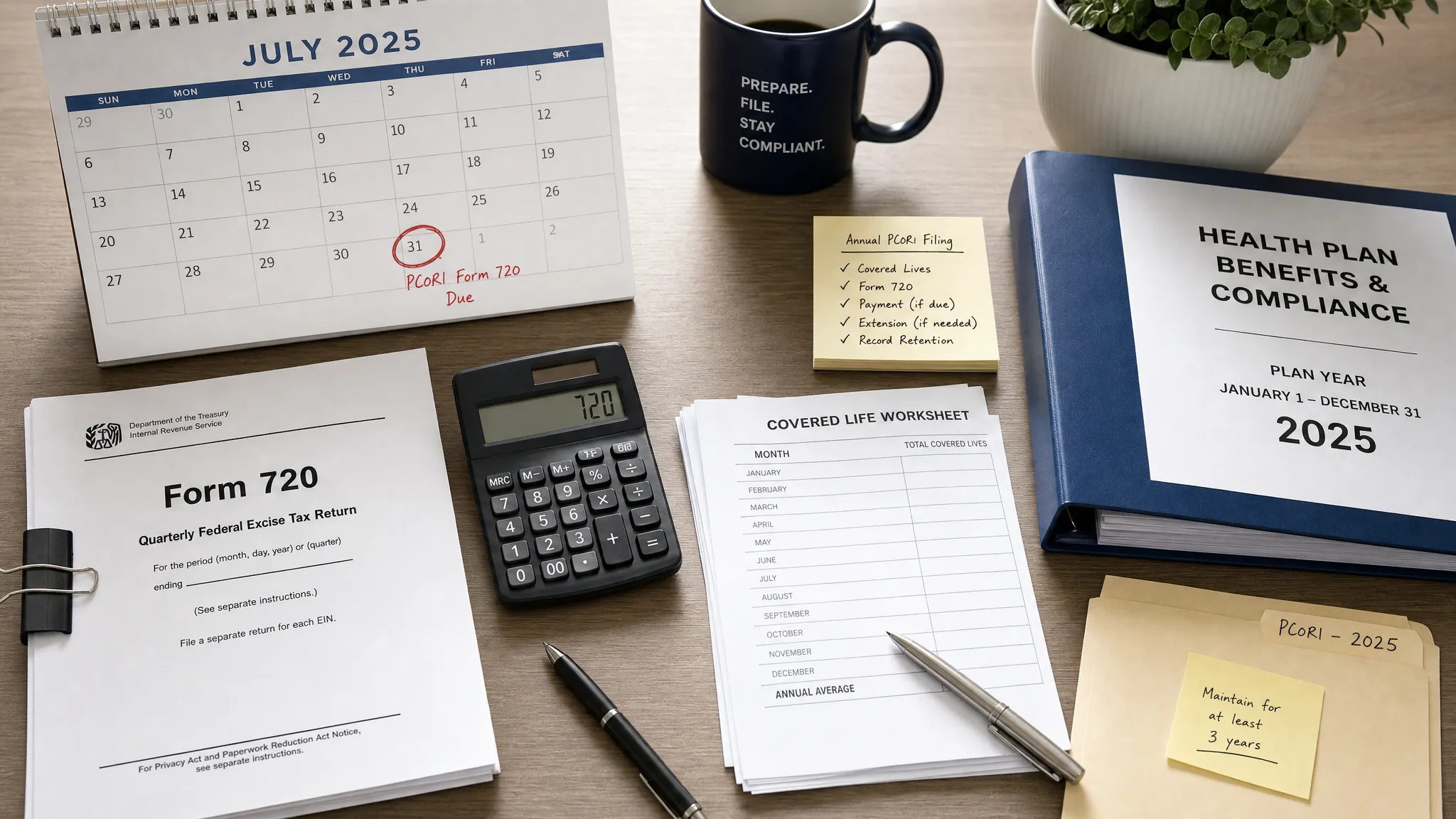

For the 2026 filing season, the key deadline is Friday, July 31, 2026, for applicable health plans and policies that ended in 2025. If you sponsor a self-insured health plan, a level-funded plan, or certain HRAs, this IRS Form 720 PCORI guide will help you confirm who files, which rate applies, how to count covered lives, and how to submit the return on time.

The IRS explains the PCORI fee in its Patient-Centered Outcomes Research Trust Fund fee questions and answers. For the mechanics of reporting it, filers should also review the current IRS Instructions for Form 720.

IRS Form 720 PCORI filing at a glance for 2026

| Filing item | 2026 PCORI rule |

|---|---|

| Main due date | July 31, 2026, for plan or policy years ending in 2025 |

| Return used | IRS Form 720, Quarterly Federal Excise Tax Return |

| Form 720 quarter | Second quarter, quarter ending June 30, 2026 |

| Where PCORI appears | Patient-centered outcomes research fee, IRS No. 133 |

| Calendar-year 2025 plan rate | $3.84 per covered life |

| Fiscal plan years ending Jan. 1, 2025 through Sept. 30, 2025 | $3.47 per covered life |

| Deposits | PCORI fees generally are paid with the return, not through semi-monthly excise deposits |

| Common responsible filer | Insurer for fully insured policies; plan sponsor for self-insured plans |

The most important point: do not use the filing year alone to choose the rate. The PCORI rate depends on the date the plan or policy year ended.

What is the PCORI fee?

The PCORI fee funds the Patient-Centered Outcomes Research Trust Fund. It applies to issuers of specified health insurance policies and sponsors of applicable self-insured health plans. Although it is reported on IRS Form 720, it is different from many other federal excise taxes because most employers only deal with it once per year.

Form 720 is commonly associated with fuel taxes, environmental taxes, communications taxes, indoor tanning taxes, and other excise categories. PCORI is reported on the same form, but it has its own annual timing. For most plan sponsors, the PCORI fee is reported on the second-quarter Form 720 due July 31 of the calendar year following the end of the plan year.

For example, a calendar-year self-insured health plan that ended on December 31, 2025, reports and pays its PCORI fee by July 31, 2026.

Who must file IRS Form 720 for PCORI in 2026?

Start by identifying whether the coverage is fully insured, self-insured, or a mix of both. The party responsible for paying and filing can change based on that funding structure.

| Coverage arrangement | Who usually files and pays | 2026 filing note |

|---|---|---|

| Fully insured major medical policy | Health insurance issuer | The employer usually does not file Form 720 for that insured policy |

| Self-insured major medical plan | Plan sponsor, often the employer | File the second-quarter Form 720 if the plan year ended in 2025 |

| Level-funded health plan | Often the plan sponsor | Many level-funded arrangements are treated as self-insured, even when a carrier or TPA administers claims |

| HRA paired with fully insured medical coverage | Employer or plan sponsor for the HRA | The insurer may report the policy, while the employer may still owe PCORI for the HRA |

| HRA paired with self-insured medical coverage from the same sponsor | Plan sponsor | Aggregation rules may help prevent double counting when arrangements share the same plan year |

| Standalone dental, vision, or other excepted benefits | Usually no PCORI fee | Confirm the benefit qualifies as an excepted benefit |

Do not assume your payroll provider, broker, or third-party administrator files the PCORI return for you. A TPA may provide covered-life data, but the plan sponsor is often responsible for filing and paying when the plan is self-insured.

If your organization has multiple health benefit arrangements, review the plan documents, funding contracts, and TPA reports before deciding who files. This is especially important for HRAs, ICHRAs, level-funded plans, multiemployer arrangements, and plans with non-calendar-year plan years.

2026 PCORI fee rates and due dates

For 2026 filing, most employers are reporting a plan year that ended at some point in 2025. The applicable rate depends on whether that plan year ended before or after October 1, 2025.

| Plan or policy year ending date | Applicable PCORI rate | When generally reported |

|---|---|---|

| Jan. 1, 2025 through Sept. 30, 2025 | $3.47 per covered life | July 31, 2026 |

| Oct. 1, 2025 through Dec. 31, 2025 | $3.84 per covered life | July 31, 2026 |

| Jan. 1, 2026 through Sept. 30, 2026 | $3.84 per covered life | July 31, 2027 |

A calendar-year 2025 plan uses the $3.84 rate because the plan year ended on December 31, 2025. A fiscal-year plan that ended on June 30, 2025, uses the $3.47 rate.

Here is a simple example. If a calendar-year self-insured plan ended December 31, 2025, and had 150 average covered lives, the PCORI fee would be 150 x $3.84, or $576. The plan sponsor would report that amount on the second-quarter 2026 Form 720 by July 31, 2026.

How to calculate average covered lives

The PCORI calculation is straightforward once you have the right count:

Average covered lives x applicable PCORI rate = PCORI fee due

The challenge is the covered-life count. For many self-insured medical plans, covered lives include employees, spouses, dependents, retirees, and COBRA qualified beneficiaries covered under the plan. For HRAs and certain account-based arrangements, special counting rules may apply.

Employers generally use one of the IRS-approved counting methods for applicable self-insured health plans. The right method depends on the quality of your enrollment data and whether you file Form 5500 by the PCORI due date.

| Counting method | How it works | When it may fit |

|---|---|---|

| Actual count method | Add the covered lives for each day of the plan year, then divide by the number of days in the plan year | Best when daily eligibility data is reliable |

| Snapshot method | Count covered lives on one or more consistent dates in each quarter, then average the results | Useful when payroll or enrollment snapshots are easier to obtain |

| Snapshot factor method | Count participants with self-only coverage plus participants with other-than-self-only coverage multiplied by the IRS factor | Often useful when dependent-level data is limited |

| Form 5500 method | Use participant counts reported on Form 5500, subject to IRS rules | Practical when Form 5500 is filed by the PCORI deadline |

| HRA special counting rule | Certain HRAs may count one covered life per employee participant, without counting dependents | Useful for HRA-only PCORI calculations |

Use one method consistently for the plan year and keep documentation showing how you reached the count. If you change methods from year to year, retain a clear explanation in your compliance file.

For insured policies, issuers have separate counting methods available. Employers sponsoring self-insured plans should focus on the self-insured plan methods in the Form 720 instructions.

Step-by-step IRS Form 720 PCORI filing checklist for 2026

Use this workflow before submitting your 2026 PCORI filing:

- Confirm the plan or policy year end date: Identify the exact date the health plan year ended. This determines both the due date and the correct PCORI rate.

- Determine the responsible filer: Confirm whether the insurer, employer, plan sponsor, or another legally responsible party must file Form 720.

- Select the correct PCORI rate: Use $3.47 for plan years ending Jan. 1, 2025 through Sept. 30, 2025, and $3.84 for plan years ending Oct. 1, 2025 through Dec. 31, 2025.

- Calculate average covered lives: Choose an IRS-approved counting method and document the source data used.

- Prepare the second-quarter Form 720: Use the quarter ending June 30, 2026, and report the PCORI fee under IRS No. 133.

- Verify the EIN and legal business name: IRS rejections and processing delays often happen when the filer name or EIN does not match IRS records.

- Submit the return by July 31, 2026: File on time even if the PCORI amount is relatively small. Late Form 720 filing can create avoidable penalties and interest.

- Pay the PCORI fee and save proof: Follow IRS payment instructions, then keep the filed return, payment confirmation, covered-life calculation, and supporting records.

If you already file Form 720 for other excise taxes, do not mix PCORI into the wrong quarter. PCORI is generally reported on the second-quarter return, even though the plan year being reported ended in the previous calendar year.

Common PCORI filing mistakes to avoid

Small PCORI balances can still create compliance issues when the wrong rate, filer, or covered-life count is used. The most common mistakes are preventable with a short pre-filing review.

| Mistake | Why it matters | How to avoid it |

|---|---|---|

| Using employee headcount instead of covered lives | PCORI often counts more than employees, including dependents and COBRA participants | Use an approved covered-life counting method |

| Applying the wrong rate | The rate depends on the plan year end date, not the date you prepare the return | Match the rate to the plan year ending date |

| Assuming fully insured rules apply to a level-funded plan | Level-funded plans are often self-insured for PCORI purposes | Review the funding arrangement and plan documents |

| Forgetting an HRA | An employer may owe PCORI for an HRA even when the medical policy is insured | Review all health reimbursement arrangements |

| Filing the wrong Form 720 quarter | PCORI is reported annually on the second-quarter Form 720 | Use the quarter ending June 30 for the annual PCORI filing |

| Relying on a TPA without confirmation | TPAs often provide data but may not be responsible for filing | Confirm responsibility in writing before the deadline |

Also be careful with acquisitions, benefit plan changes, and mid-year plan terminations. If a plan year ended in 2025, the PCORI filing may still be due in 2026 even if the arrangement is no longer active.

What records should you keep?

Keep a PCORI workpaper file with the plan year dates, plan documents, funding status, covered-life source reports, counting method, rate used, final calculation, filed Form 720, payment proof, and any TPA or broker correspondence supporting the count. For Form 720 excise tax records, businesses generally should retain records for at least four years.

Good records matter if you later discover an error. If you underreported the fee, you may need to correct the filing and pay the additional amount. If you overreported, review the current IRS instructions for the proper correction or claim process. eFileExcise720 supports Form 720 amendments through Form 720-X, and also supports Form 8849 claims where applicable.

Can you e-file the PCORI fee on Form 720?

Yes. Form 720 can be filed electronically through an IRS-authorized e-file provider. E-filing helps reduce manual entry issues, provides electronic submission confirmation, and can be especially useful for organizations that do not file Form 720 every quarter.

eFileExcise720 is an IRS-authorized online platform for Form 720 e-filing. You can create an account, prepare your return without downloading software, navigate a simple dashboard, and submit securely. The platform supports all Form 720 categories, including PCORI, and offers personalized customer support for filers who need help completing their return.

If you are still confirming whether your organization is responsible for the fee, you can also review this related guide on who is required to pay the PCORI fee. For a broader annual preparation list, see the Form 720 e-filing checklist for 2026.

Frequently Asked Questions

What is the IRS Form 720 PCORI deadline for 2026? The main 2026 PCORI filing deadline is July 31, 2026, for applicable plans and policies that ended in 2025. Because July 31, 2026, falls on a Friday, the standard deadline applies.

What PCORI rate should a calendar-year 2025 plan use? A calendar-year 2025 plan ended on December 31, 2025, so it uses the $3.84 per covered life rate for the Form 720 due July 31, 2026.

Is the PCORI fee filed every quarter? No. Although Form 720 is a quarterly excise tax return, the PCORI fee is reported annually, generally on the second-quarter Form 720 due July 31.

Does an employer file PCORI for a fully insured health plan? Usually, the insurance issuer files and pays the PCORI fee for a fully insured policy. However, the employer may still need to file if it sponsors a separate self-insured arrangement, such as certain HRAs.

Do PCORI fees require semi-monthly excise tax deposits? PCORI fees generally are paid with the Form 720 return rather than through the semi-monthly deposit rules that apply to many other excise taxes.

What happens if I miss the July 31 PCORI deadline? File and pay as soon as possible. Late filing, late payment, and interest may apply. If you have a reasonable cause explanation, review IRS guidance or consult a tax professional about penalty relief options.

Ready to file your 2026 PCORI Form 720?

If your organization needs to report the PCORI fee for a 2025 plan year, do not wait until the last week of July to gather covered-life data. Confirm the filer, rate, count, and payment plan now so the return is ready before the deadline.

You can file your Form 720 online with eFileExcise720 through an IRS-authorized, secure e-filing portal built to make excise tax compliance faster and easier. Create your account, prepare the PCORI filing, and submit your return with support available when you need it.